The majority of insurance companies need preauthorization prior to concurring to cover a visit to a professional. Preauthorization doesn't guarantee a service will be covered. Instead, it confirms that the insurance company intends to cover the service pending review of the claim and determinating the service was necessary. Many non-critical treatments require preauthorizations. And it's typically the insurance policy holder's duty to know if preauthorization is required. Failure to get preauthorization can result in a claim rejection. Pay unique attention to the preauthorization requirement when seeing an expert at the suggestion of your main physician. Lots of main caretakers are in-network but might unwittingly refer patients to an out-of-network specialist.

Insurance companies generally send out a description of a medical claim's payment after it's adjudicated or approved. This explanation of advantages, or EOB, generally describes what was covered and what might have been left out. It likewise details the last contracted costs for the service, the proportion of the costs paid by the insurer (and the quantity which stays the client's responsibility), and a description of how the various quantities were determined - How does life insurance work. Constantly examine an EOB to identify whether the insurance provider's payment matches your understanding of the policy. Many health insurance providers count on older legacy details systems to review and make claim payments. Insurance companies are generally big governmental organizations with several levels of management. A good outcome might require weeks, or even months, to be completely settled, so ensure average cost of timeshares to document every action of the process. Escalate your request to higher-ups if you face an obstruction, a hostile agent, or a choice you disagree with. A letter to the president of the insurance provider and your state's insurance coverage commissioner will create activity on your claim, but you ought to just utilize it as a last hope. If and when a mistake takes place, keep in mind that the workers at the insurer might be simply as bewildered as you are.

Excellent health is your most precious asset, and you must secure it at all expenses. The worth of medical insurance can not be overemphasized. Being without medical insurance can result in delayed treatment, numerous thousands of dollars in expenses, and even personal bankruptcy in case of an accident, major disease, or persistent condition. Protect yourself and your family by being an informed purchaser of health insurance that fits your particular needs. What about medical insurance puzzles you?.

You can choose from a range of medical insurance prepares with different levels of coverage to fit your requirements and budget. Let's say you've had a severe mishap. Your medical bills are $50,000. Medical insurance may make a substantial difference in the quantity you'll pay. In this example, all the care you get is from medical professionals how to legally get rid of a timeshare and healthcare facilities in your strategy network. * Annual deductible: $5,000 Coinsurance: 20% Annual out-of-pocket optimum: $6,000 In this example, you pay the first $5,000 (your deductible) prior to your plan starts to pay. After you pay the deductible, you pay 20 percent of your healthcare expenses until you reach your maximum out-of-pocket quantity ($ 6,000).

Once you've paid $6,000, your health plan pays the rest of the expense for covered services you get in network. Bill for services: $50,000 You pay: $6,000 Your strategy pays: $44,000 Coinsurance: The percent of the cost you pay for covered services. For example, you pay 20 percent of the expense for a medical professional's office visit or medical facility stay. Your strategy pays the other 80 percent. Not all strategies include coinsurance. Copay: A small, flat cost you spend for some covered care at the time of service (for instance, $25 for an office visit). Some plans do not need a copay.

To discover what your plan covers, log into the member site, call the number on the back of your ID card or examine the agreement in your member welcome set. Deductible: The quantity you spend for healthcare each year prior to your strategy begins to pay. A list of drugs your plan covers. If you fill a prescription for a drug your strategy does not cover, you'll pay the complete expense. This expense will not count towards your deductible or out-of-pocket maximum. How to comprehend prescription drug benefits Before-tax contributions you make to an HSA account. You can utilize HSA funds to pay for some covered health care costs.

These are also referred to as getting involved or in-network providers. To get the most protection, you get care from suppliers in your health insurance network and drug stores in your plan's drug store network. Some service providers or pharmacies might not remain in a strategy's networks. Providers or drug stores in one network might not be in another network. Some strategies have a focused network. A concentrated network implies that only particular service providers or pharmacies take part in the strategy's service provider or https://www.onfeetnation.com/profiles/blogs/9-easy-facts-about-when-is-open-enrollment-for-health-insurance pharmacy networks. If you visit a supplier or a location that is not in the strategy network, you will pay more for your care.

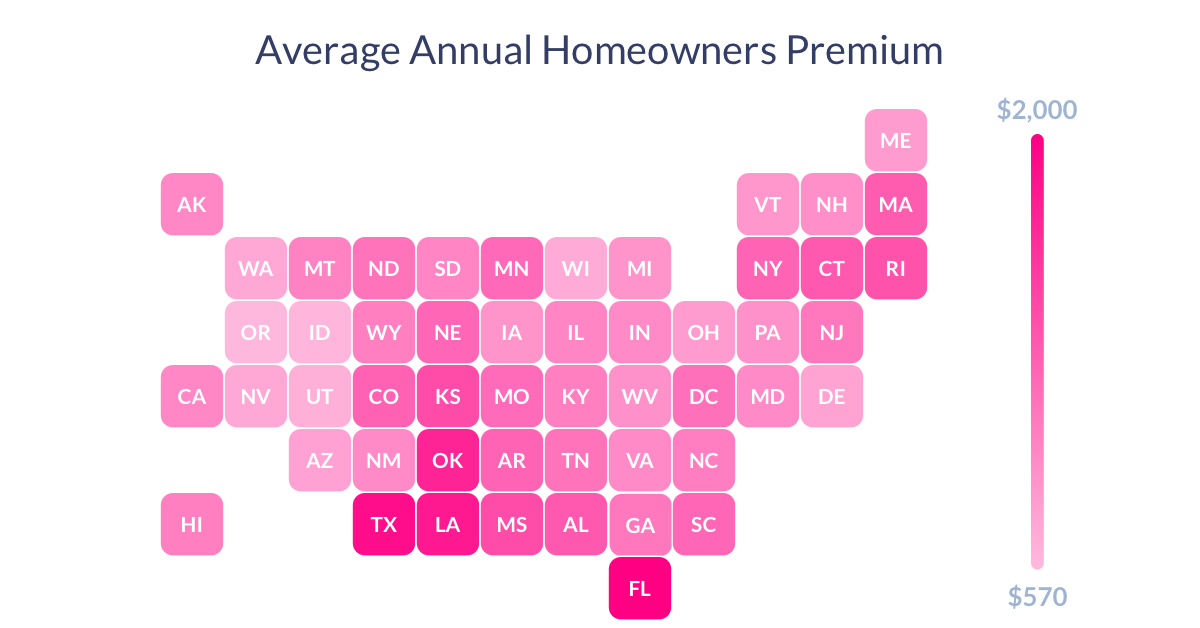

Facts About What Is Homeowners Insurance Uncovered

These out-of-network costs do not count toward your in-network cost-sharing (for example, your deductible and out-of-pocket optimum). Out-of-pocket maximum: The most you could pay each year for covered services you receive in network. Premium: The monthly quantity you pay for your health plan. Usually, a lower premium features a greater deductible and out-of-pocket optimum.

Health insurance is a kind of insurance coverage that covers the whole or a part of the threat of an individual sustaining medical expenditures. As with other kinds of insurance is risk among lots of people. By approximating the total danger of health threat and health system expenditures over the risk pool, an insurance provider can establish a routine financing structure, such as a regular monthly premium or payroll tax, to offer the cash to pay for the healthcare benefits specified in the insurance coverage contract. The benefit is administered by a main organization, such as a federal government agency, private organization, or not-for-profit entity.

It includes insurance for losses from mishap, medical cost, impairment, or unexpected death and dismemberment".:225 A health insurance policy is: A contract between an insurance service provider (e. g. an insurance business or a government) and an individual or his/her sponsor (that is an employer or a community organization). The contract can be sustainable (yearly, monthly) or long-lasting when it comes to private insurance coverage. It can likewise be mandatory for all citizens in the case of nationwide strategies. The type and amount of health care expenses that will be covered by the health insurance provider are defined in writing, in a member agreement or "Evidence of Protection" pamphlet for private insurance, or in a national [health policy] for public insurance coverage.